Out-of-the-box

Solution

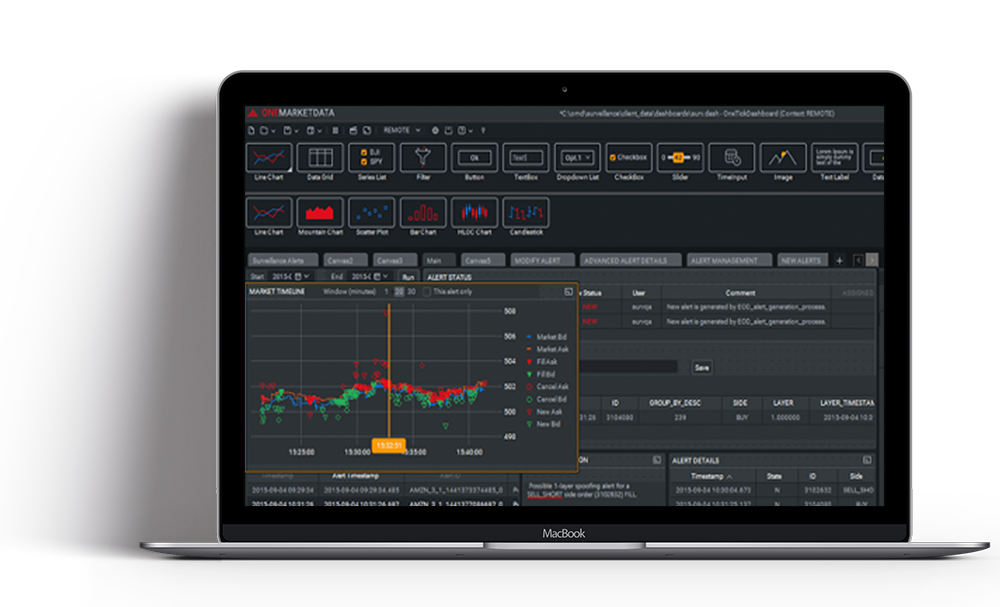

Intra-day and T+1 monitoring of transactions flow with immediate and worked orders support, advanced visualizations, alerting, filtering, and outlier management, aggregate reporting, and compliance workflow.

When deployed on-premises, OneTIck BestEx supports closer integration with customer infrastructure and proprietary data sources, supports intra-day monitoring, and allows integration of customer-developed metrics.

OneTick BestEx supports end-user creation of additional metrics and statistics by means of a configurable window that allows limited scripting right in the Best Ex dashboard.

Metrics may be created that are simple or complex functions of any other data columns present in the enriched data. Complex filters may also be created using the code widget. For example, it might be used to create a venue ranking formula that is based on a combination of venue-relevant execution quality metrics and market statistics.

Empower your quantitative research and trading with OneTick's precision data & analytics today!